NAVIGATING THE EU CARBON BORDER ADJUSTMENT MECHANISM

For companies that move early, the EU's Carbon Border Adjustment Mechanism (CBAM) is more than a new carbon pricing requirement

Meet your CBAM obligations with our suite of services

CBAM Authorised Declarant Registration

From 1 January 2026, EU companies importing covered goods must hold authorised declarant status in order to release those goods into the EU market. The registration deadline was 31 March 2026. Late registration is still possible, but companies no longer have a grace period for importing while their application is processed and past unauthorised imports may carry penalty exposure. Our team can help you navigate late registration and resume importing as quickly as possible. Authorised declarant status is now a baseline requirement for doing business in the EU.

Embedded Emissions Calculation & Verification

CBAM requires importers to purchase and surrender certificates based on verified embedded emissions. Default values are permitted where supplier data is unavailable, but they are deliberately conservative and getting more expensive. We help clients calculate actual emissions to keep certificate costs as low as possible. Verified data directly reduces your certificate costs — and the savings compound as default values increase each year.

CBAM Declaration & Certificate Management

The first annual CBAM declaration covers goods imported during 2026, with a surrender deadline of September 30th, 2027. Starting in 2027, importers must hold certificates covering at least 50% of embedded emissions at each quarter-end. We manage the full declaration lifecycle and advise on certificate purchasing strategy. A proactive certificate strategy protects cash flow and keeps you ahead of quarterly holding requirements.

Supply Chain CBAM Readiness

CBAM obligations fall on EU importers, but they depend on accurate emissions data from their upstream suppliers. For non-EU exporters, providing verified data on time is essential to maintaining EU customer relationships. We work with both importers and suppliers to build reliable data pipelines. EU importers are already building preferred supplier lists — suppliers who can deliver verified emissions data have the edge; those who can't risk being replaced.

Understand when and how CBAM obligations affect your company

Why Early Movers Win

Reduce certificate costs

Verified data beats default values on day one, and the gap grows every year

Strengthen EU customer relationships

EU importers are building preferred supplier lists now; data-ready partners have the edge

Signal carbon leadership

CBAM compliance demonstrates the kind of supply chain transparency that investors and frameworks like CDP increasingly reward

CBAM is already in effect. Companies that invest in accurate emissions data now will not only reduce their compliance costs but also position themselves as preferred partners in an EU market that is increasingly rewarding carbon transparency.

Annie Roberts

Senior Vice President - Climate ConsultingUnderstanding CBAM

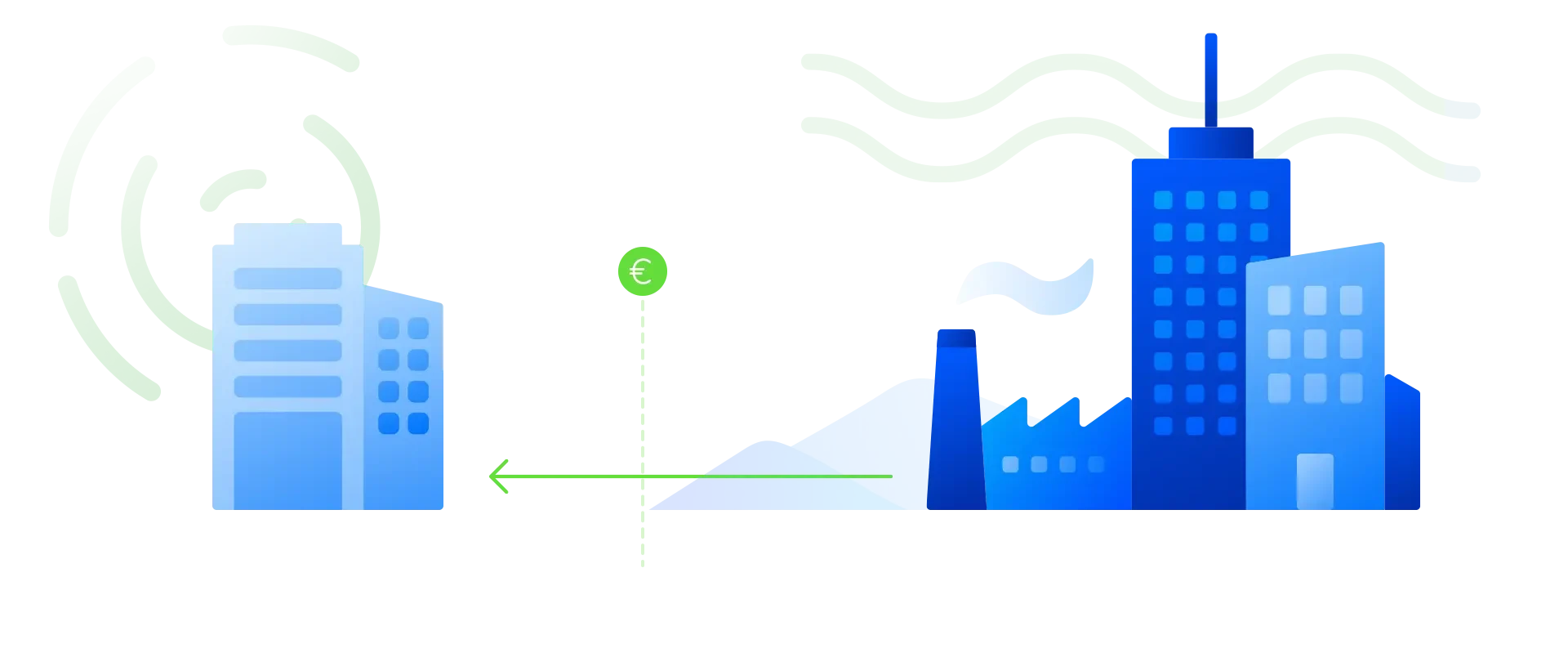

The CBAM is an EU policy that places a carbon cost on certain goods imported into the EU, mirroring the carbon price already paid by EU producers under the EU ETS. It is designed to prevent “carbon leakage,” which is where importers source goods from countries with less stringent climate rules, undercutting domestic producers who bear the cost of emissions compliance.

CBAM directly applies to EU importers of covered goods, but its effects extend across supply chains. Non-EU exporters, including U.S.-based companies, face indirect pressure: EU importers cannot surrender certificates without supplier emissions data, meaning suppliers who cannot provide it risk being replaced.

CBAM currently applies to six sectors. For cement, iron and steel, aluminium, and fertilisers, the threshold is 50 metric tons of imports per year. Electricity and hydrogen have no threshold, meaning all importers are covered regardless of volume.

Companies must report the type and quantity of covered goods by CN code, direct and indirect embedded GHG emissions, country of origin and production facility details, manufacturing processes used, precursor materials, and any carbon price already paid in the country of origin.

Each CBAM certificate represents one tonne of CO₂ equivalent (CO₂e) embedded in imported goods. The price is calculated based on the auction price of EU ETS allowances expressed in €/tonne of CO₂ emitted, as a quarterly average in 2026, and as a weekly average from 2027 onwards. Certificates must be surrendered by September 30th each year, beginning in 2027.

Default values are calculated using the average emissions intensity of the ten highest-emitting exporting countries — meaning they are deliberately set high to create a compliance incentive. If your suppliers operate more efficient or cleaner facilities than that average, using defaults means you are overpaying for certificates you do not owe. That cost gap grows each year: default values increase by 10% in 2026, 20% in 2027, and 30% from 2028 onward. Investing in actual, verified emissions data now protects your cost position as CBAM matures — and companies that build this capability early are better positioned as preferred supply chain partners in an EU market that is increasingly rewarding carbon transparency.

Yes. If a carbon price has already been paid in the country where goods were produced, importers can deduct that amount from the certificates they are required to surrender, preventing double taxation across the supply chain. Supporting documentation must be included in the annual declaration.

Verification can only be provided by entities accredited by a National Accreditation Body (NAB) of an EU member state. Verification entities already accredited under the EU Emissions Trading System (EU ETS) are likely to be among the first to obtain CBAM accreditation.

Let's start a conversation.

Related Services

Explore what else G&A can offer

Understand what’s shaping sustainability.

Dive into blog posts that break down trends and emerging issues.

Explore the Blog