Key Highlights

- California's SB 253 and SB 261 have created a climate disclosure framework that other states are actively using as a policy template.

- Five states — New York, New Jersey, Colorado, and Illinois — have introduced legislation mirroring California's emissions and financial risk reporting requirements.

- The absence of a clear federal baseline from the SEC has accelerated state-level climate disclosure activity, making multi-jurisdiction compliance increasingly complex.

- Companies can get ahead by clarifying data ownership, building scalable emissions data processes, and tracking state legislative developments as they unfold.

California’s recently enacted climate disclosure laws have become an important reference point for companies that report, or may soon be expected to report, climate-related information. Even though implementation timelines and legal challenges are still playing out, the direction is clear: U.S. states are venturing into corporate climate disclosure requirements, and California’s framework is influencing what those proposals look like.

This article summarizes the purpose and core structure of California’s laws, then reviews proposed legislation in other states that could mirror key elements of SB 253 and/or SB 261. The goal is not to predict which bills will pass, but to help companies spot patterns and pressure points early, especially if they operate nationally.

Recent state-level developments suggest that climate disclosure is becoming based less on isolated mandates and more on a shared set of expectations that companies will need to navigate across jurisdictions. As more states introduce legislation modeled on California’s approach, organizations may find increasing similarities in how emissions data and climate-related financial risks are evaluated.

Climate disclosure is becoming based less on isolated mandates and more on shared expectations across jurisdictions.

California as a Reference Framework for State Action

California’s climate disclosure framework, also referred to as the “Climate Accountability Package,” centers on two laws:

- SB 253 (Climate Corporate Data Accountability Act): Requires certain large companies doing business in California to publicly disclose Scope 1, Scope 2, and Scope 3 greenhouse gas (GHG) emissions

- SB 261 (Climate-Related Financial Risk Act): Requires certain large companies doing business in California to publish a climate-related financial risk report describing material climate risks and the measures adopted to mitigate and adapt to those risks

Implementation details for SB 253 and SB 261 are being developed by the California Air Resources Board (CARB), including reporting formats, verification requirements, and registry infrastructure.

Why have new laws from this one state attracted so much attention? We see three major reasons. First, given California’s market size, its regulatory posture and requirements can mean the state functions as a de facto baseline for wider economic expectations.

Second, when it comes to climate-related reporting, the laws’ focus on emissions data and financial risk do not seem out of step; instead it reflects growing interest among regulators and investors in understanding how climate issues may affect long-term performance and resilience.

Third, California’s climate leadership extends beyond state regulation. Governor Gavin Newsom’s participation and message at the UN Climate Change Conference in Brazil in 2025 (COP30) underscored how the state has positioned itself as a climate policy leader amid federal uncertainty. Specifically, ongoing uncertainty surrounding the U.S. Securities and Exchange Commission’s climate disclosure rule, including litigation challenges and the SEC’s decision to withdraw its defense of the rule, has left companies without a clear federal baseline. California’s assertive positioning in the absence of national clarity helps explain why other states may view climate disclosure not only as a regulatory exercise, but as part of a larger governance strategy.

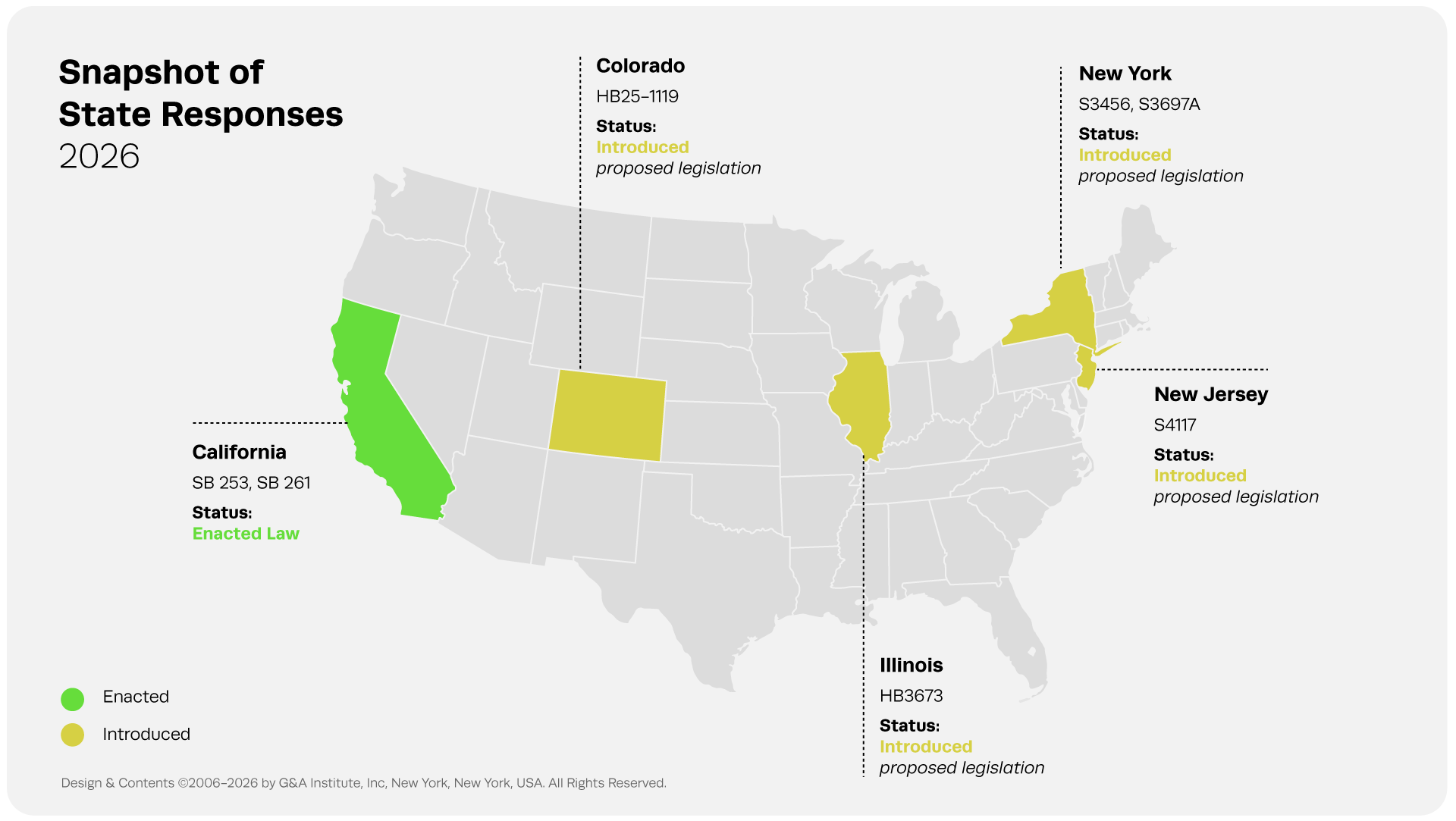

Snapshot of State Responses and Emerging Legislative Patterns

Several states have introduced legislation with echoes of California’s approach. This table provides key details from the four states’ proposals as well as the California bills, comparing their signals on: revenue threshold, Scopes 1, 2, and 3 emissions inventories, timing, and other requirements.

Key details:

| State | Bill(s) | Covered Companies | Required Disclosures | Timing (as written) | Assurance / Other Details |

| California | SB 253

Status: Enacted law |

Companies doing business in CA with >$1B revenue | Annual disclosure of Scope 1–3 emissions | Phased, beginning 2026

|

Requires phased third-party assurance of Scope 1 and 2 emissions beginning in 2026 (limited assurance), increasing to reasonable assurance by 2030. Scope 3 reporting is phased in, with potential limited assurance requirements expected around 2030, subject to CARB rulemaking.

|

| California | SB 261

Status: Enacted law |

Companies doing business in CA with >$500M revenue | Biennial climate-related financial risk report aligned with TCFD, IFRS S2, or other accepted frameworks | First reports expected 2026–2027 | No third-party assurance requirement. Requires biennial disclosure of climate-related financial risks aligned with recognized frameworks such as TCFD or IFRS S2. |

| New York

|

S3456

Status: Introduced (proposed legislation) |

Entities doing business in NY with >$1B annual revenue

|

Annual disclosure of Scope 1-3 emissions, aligned with the Greenhouse Gas Protocol | Tiered implementation, beginning 2027 | Authorizes third-party assurance of emissions data and allows phased implementation structure similar to SB 253.

Covered companies, reporting requirements, and timing subject to change as the legislative process unfolds. |

| New York | S3697A

Status: Introduced (proposed legislation) |

Entities doing business in NY with >$500M annual revenue

|

Biennial climate-related financial risk disclosure aligned with TCFD or similar frameworks | First risk report due January 1, 2028 | Requires disclosure of climate-related financial risks and reporting gaps, including steps to improve data completeness over time.

Covered companies, reporting requirements, and timing subject to change as the legislative process unfolds. |

| New Jersey | S4117

Status: Introduced (proposed legislation)

|

Entities doing business in NJ with >$1B annual revenue for the prior fiscal year | Annual disclosure of Scope 1–3 emissions to a state registry and the NJ Department of Environmental Protection (NJDEP) | Phased public disclosure, beginning three to five years after effective date | Requires phased third-party assurance for Scope 1–2 emissions.

Covered companies, reporting requirements, and timing subject to change as the legislative process unfolds. |

| Colorado | HB25-1119

Status: Introduced (proposed legislation)

|

Entities doing business in CO with >$1B annual revenue for the prior fiscal year

|

Public disclosure of Scope 1–3 emissions (phased) | Scope 1–2 reporting begins Jan. 1, 2028; Scope 3 begins Jan. 1, 2029 | Legislative summary specifies phased timing structure.

Covered companies, reporting requirements, and timing subject to change as the legislative process unfolds..

|

| Illinois | HB3673

Status: Introduced (proposed legislation) |

Entities doing business in IL with >$1B annual revenue for the prior fiscal year | Annual disclosure of Scope 1–3 emissions, aligned with the Greenhouse Gas Protocol, to a state emissions registry

|

Rules due July 1, 2026; reporting begins January 1, 2027 | Requires Scope 1–3 emissions disclosures, with independent verification through the state registry or an approved third-party auditor. Registry establishes a public digital reporting platform; Attorney General enforcement authority.

Covered companies, reporting requirements, and timing subject to change as the legislative process unfolds. |

Motivations Behind State-Level Climate Disclosure Laws

Amid uncertainty around federal climate disclosure requirements and the absence of a clear national baseline, some state legislatures are advancing proposals that reflect shared policy motivations. Even though the specific mechanics differ, we see that across these proposals, the “why” tends to be consistent:

- Investors and capital markets: Legislators frequently cite demand for comparable, decision-useful climate data, especially where disclosures are voluntary or inconsistent.

- State governments and regulators: States seek clearer visibility into emissions and climate risk exposure within their jurisdictions, including impacts on infrastructure, public health, and economic planning.

- Consumers and communities: Public posting requirements suggest an intent to make disclosures accessible beyond investors, enabling stakeholders to evaluate climate commitments and exposure.

- Companies operating across jurisdictions: Fragmented reporting expectations increase compliance complexity, prompting organizations to build scalable governance, data collection, and internal control processes.

Considerations for Companies Looking Ahead

If a company operates in (or sells into) multiple states, it faces a practical challenge in building a repeatable process for data, controls, and internal sign‑off. Three near‑term moves are likely to pay off if any of the above proposals advance:

- Clarify ownership: Decide who owns emissions data (often Sustainability, EHS, or Real Estate) and who owns assurance-ready controls and disclosure (often Finance or Legal). Set up a clear review chain.

- Build data that scales: Develop a structured approach to collecting, standardizing, and documenting climate-related data so information can be reused across jurisdictions, reporting frameworks, and assurance processes. Scope 3 may need additional time and attention, requiring supplier mapping, calculation methodologies, and clear documentation of assumptions.

- Track state activity: Use each state’s legislative decisions to inform your company’s plans for expanding data coverage, piloting assurance, and upgrading systems.

In short, companies should bolster their climate-related governance, cross‑functional coordination, and ongoing monitoring.

The California Impact: A New Corporate Standard

California’s SB 253 and SB 261 have created a policy template that other states are drawing from as they develop their own climate disclosure requirements.

New York’s pair of proposals show how emissions reporting and financial risk reporting can move in parallel, New Jersey’s approach exhibits phased public posting and assurance, Colorado’s bill is explicit on start dates, and Illinois adds detail on registry infrastructure and verification.

Taken together, these proposals suggest a growing expectation that large companies will produce emissions inventories (including Scope 3) and explain how climate risk can affect financial outcomes, even as exact rules may vary state to state.

Where to Start

Founded in 2006, Governance & Accountability Institute (G&A) is a New York–based sustainability consulting and research firm advising corporate leaders and investors at the intersection of strategy, governance, and regulation. For two decades, we have partnered with executive teams and boards to translate sustainability strategy into durable enterprise value — helping organizations navigate shifting market expectations, evolving policy landscapes, and increasing capital markets scrutiny. Set up a call to learn more about how we can help your company.

Share This Article

How Can G&A Help?

How Can G&A Help?

Build your sustainability strategy.

Chat with our experts to get started on your journey.

Get Started